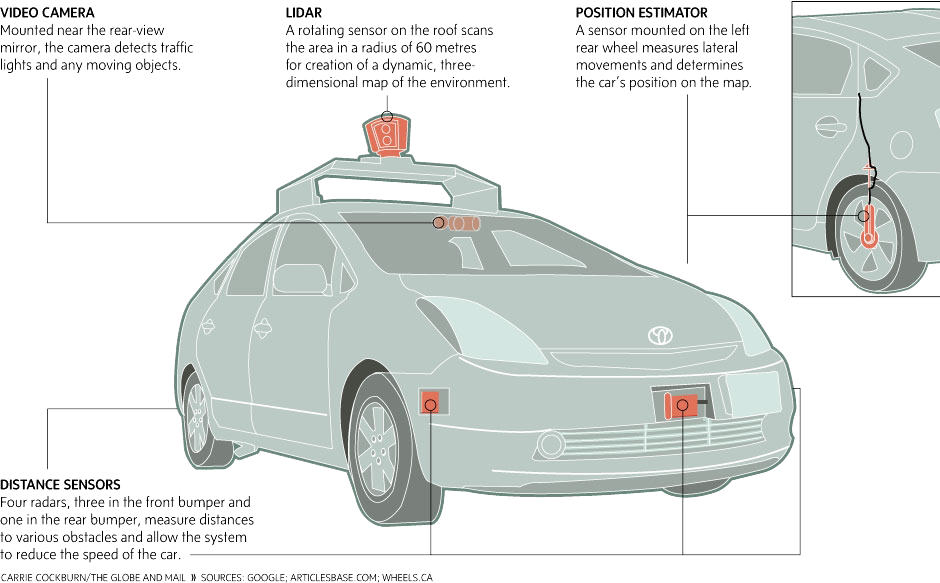

Google is famous as the world’s most used search engine, for its Google Earth mapping system, Gmail, and many other things that you can bring up on your computer or portable device. Google has recently been investing in a multitude of companies to increase their umbrella. One of its most talked about projects at the moment is its driver-less car.

Once your destination has been set in the car you can read a book, watch a tv show, or even sleep while the car delivers you to the destination. There is an option to override the Google car system but when you do that, watch out; the only times these cars have ever been in an accident were when a human was driving it. Every mile driven without a driver has been a safe one. Google is not alone in the quest to build a driverless car. BMW, Toyota, Nissan, and General Motors are also developing self-driving cars, though Google appears far ahead of others.

How Will Driver-less Cars Affect the Future?

More than 90 percent of all auto accidents result from driver error. It might be due to drowsiness, distracted driving, or other reasons, and inventors are hard at work trying to end needless fatalities with smart cars. Right now, in 2014, cars come with possible life-saving technology that detects problems and avoids accidents. It is only a matter of time before the driver is gone from the equation.

Today your car may already be equipped with:

- Lane-drifting Alarms

- Rearview Cameras

- Technology to assure driver sobriety before allowing the car to start

- Seat vibrators to warn drivers of Impending danger

The Benefits of Driver-less Cars

- Fewer accidents Less injuries and fatalities

- Lower insurance rates for all

- Increased fuel economy

Auto industry analysts believe Americans will see this technology offered as soon as 2018. However, will America be ready? Presently, Nevada, California, Michigan, Florida, and Washington, D.C., have laws that govern driverless automobiles. However, these laws are for safety and regulating their on-road use. Auto insurance issues are still up in the air.

Driverless Cars and Their Effect on Auto Insurance

Many believe that when driver-less cars become ubiquitous on our roads, the effect on the profitability of insurance companies will shrink profits. Donald Light, Director of Americas Property/Casualty Insurance Practice at financial technology consulting firm Celent, said:

“Innovations could lead to decreases in car insurance premiums by more than 60 percent in the 2020s from current levels. The advances include the increasingly prevalent driver-monitoring devices, collision avoidance systems and automated traffic-law enforcement, such as speed and red-light cameras, as well as robotic cars.â€

If driverless cars become popular, car owners still need comprehensive coverage. This coverage might only cover damage from incidents not involving another car, but perils such as fire, explosions, fallen trees, theft, earthquakes, and riots. Premiums, however, are risk related; the higher the risk, the higher the premium. If risks decrease due to improved safety of autonomous cars, then premiums go down.

Because of the proven safety of driverless cars, some insurance analysts predict that plummeting premiums will cause insurance companies’ profits to fall dangerously low. Others say that will not happen. Carol Csanda, Innovation Team Director with State Farm, believes that new car insurance products will come about for new situations. State Farm is working with Ford and the University of Michigan, attempting to “identify new risks as they emerge,†according to Csanda.

Most believe that it is too soon to understand the impact on insurance from the development and deployment of driverless cars. Nevertheless, as added technology has stabilized and reduced insurance premiums, it seems that the trend is for premiums to fall when driverless car ownership becomes common.

The information in this article was obtained from various sources. This content is offered for educational purposes only and does not represent contractual agreements, nor is it intended to replace manuals or instructions provided by the manufacturer or the advice of a qualified professional. The definitions, terms and coverage in a given policy may be different than those suggested here and such policy will be governed by the language contained therein. No warranty or appropriateness for a specific purpose is expressed or implied.